During my four years working in Hong Kong and Beijing, I couldn’t help but feel that I missed the proverbial boat for investment into the Chinese market. Over those four years, I regularly met with fellow foreign businessmen who’d been doing business in China for decades. Many had lived in China for a majority of their working lives. They talked about their successes and failures, businesses won or lost. In the end, no matter how many failures they had, the successes – and magnitude of those successes – far outweighed the toil of those failures.

A common theme arose in those conversations: the vast majority of their successes seemed to be businesses that were started many years ago – most often decades earlier – and many at the time that China was experiencing a flux of economic liberalization in the 1990s and early 2000s. They had captured the moment.

China was a different place when I was there compared to the opportunistic landscape that existed a few decades prior. The men I would talk to were generally older – usually 25+ years older than myself. They no longer looked to begin new enterprises within China’s borders. Rather, they maintained the existing fiefdoms they had created many years before or looked to sell them to the largest bidder. I saw more and more older, foreign executives and entrepreneurs leaving the country and less and less of their younger brethren coming to take their place.

Within my own specialty of financial services, I saw very few “new” players coming to the Chinese market. The largest banks, insurers and asset managers already had some kind of an existing operation in the market, most likely for decades. China was no longer a new concept or an unexplored blue sky territory that promised unforeseen rewards to the bold and daring. China was and is a competitive marketplace, is tightly regulated and is frankly not easy to operate in. During my time there, capital was overly abundant and large corporations dominated the investment space with nearly limitless treasure chests. In my eyes, the years of significant investment arbitrage for the individual entrepreneur were coming to an end just as my time there was beginning. That said, new markets have to give way to new capital as other markets become highly developed.

The idea of exploring an unknown land, making it one’s home, and immersing oneself into some kind of capitalistic endeavour within this new world has always excited me. I’ve always wanted that challenge for myself. Many of the conversations I had in Beijing specifically added fuel to the flames of these desires. When I listened to the stories of failures and success, I always thought to myself “if I was here 20 years ago, I would have stayed.” Arriving late, I had to find a new market that reflected the potential for growth that China previously offered.

My next chapter turned from China to Colombia, and I think it was at exactly the right time for the next investment boom.

Almost all our readers would recognize the China Boom as likely the most prevalent or at least one of the most well-known investment transformations during any of our existing lifetimes. During its peak, American companies believed it was nearly impossible not to make a fortune in this new semi-capitalistic world that China offered. Whether one believes my assessment that the arbitrage nature of this boom is at an end or not doesn’t really matter. Most booms can’t last 40+ years. At some point, the market becomes efficient and/or capital becomes too abundant and arbitrage becomes much harder to achieve. One is likely safe to argue that we are at the tail end of the boom either way. The logical question for investors is: Where is the next big macroeconomic investment opportunity?

Latin America now offers a similar opportunity for return on investment that China offered several decades ago. I see it every day.

The purpose of this article is to draw parallels between the Chinese market during its high growth period and the Latin American market of today for the individual investor. The macroeconomic similarities are there, including the onset of more formalized investment groups and capital deployment.

We will frame the conversation around what this means in terms of investment opportunities for the individual investor.

LATAM Has Earned the Right to Receive Investment Dollars

Softbank recently explained their rapid deployment of capital into LATAM through their two Latin America Funds totaling $8 billion. As the charts below show, LATAM now has a GDP per capita equal to that of China and about half the population yet received, on average during 2018-2020, only 5% of the investment dollars that China received over that same period – $82 billion (USD) for China versus only $4 billion (USD) for LATAM. If the populations of these regions are equally as productive, why are they not receiving proportionate capital allocations?

To add to the point, the charts also compare capital investment in LATAM versus investment in India and Southeast Asia. LATAM GDP per capita substantially exceeds the GDP per capita in both India and Southeast Asia yet the money going into those markets are multiples on the investment coming into LATAM in recent years. There is a misalignment here between where capital is flowing and the countries from which goods and services are coming if the goal is to create the highest likely return on a per Dollar basis.

Source: SoftBank Group presentation, Javier Villamizar, Operating Partner, Softbank Investment Advisers, Colombia Investment Summit, October 20, 2021.

Herein lies the contradiction, what is it about the Chinese market that justifies 20x the amount of smart money chasing opportunity in China vs. Latin America in recent years? Is that discrepancy reasonable? Softbank doesn’t think so and nor do we. Investors are starting to see this, and the chance to participate is still there for you.

The Latin American Investment Boom Has Begun

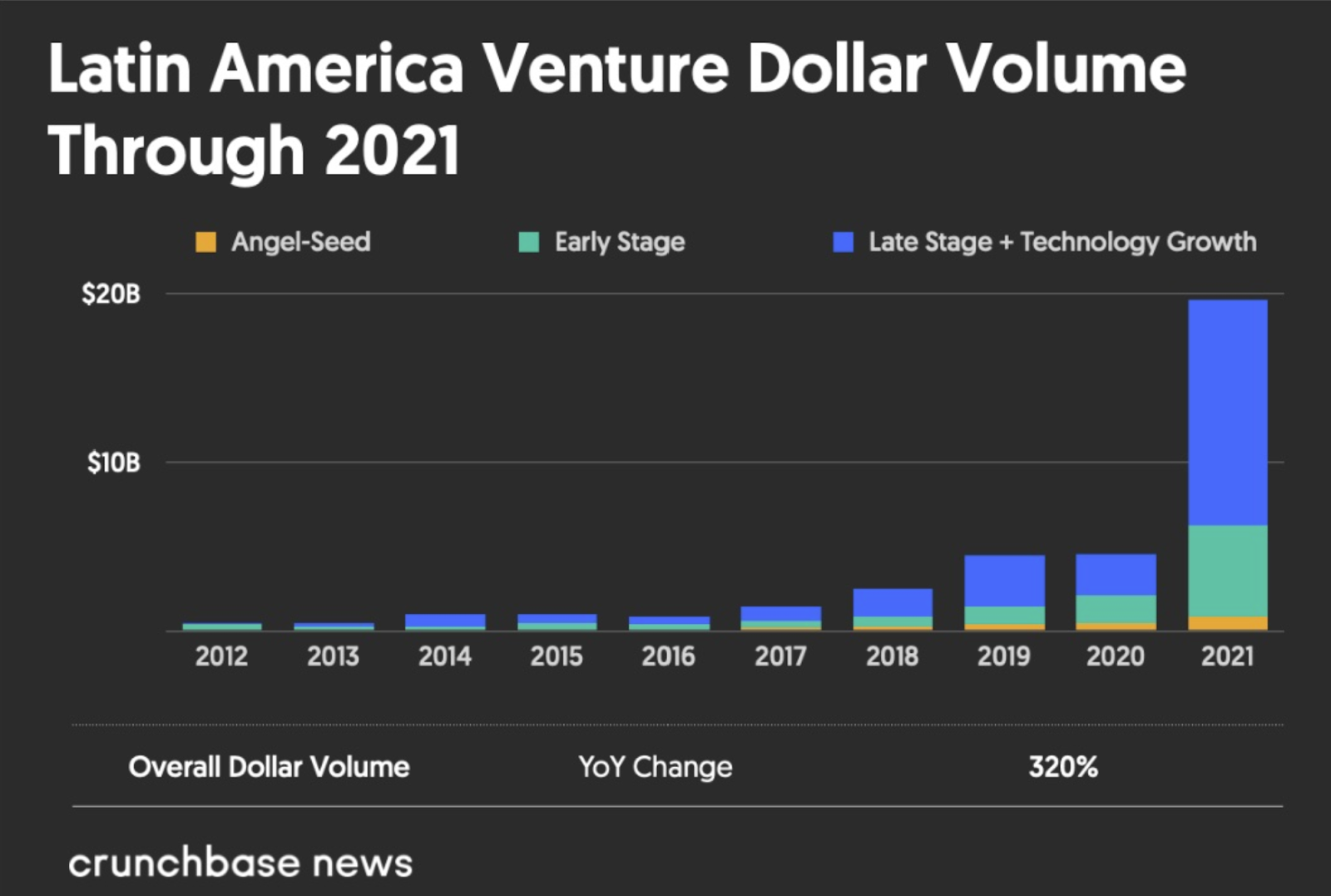

As documented by Crunchbase, Latin America broke all kinds of records related to capital investment in 2021. Most importantly, you will see in the chart below that the region funded nearly $20 billion in venture capital deals during 2021, nearly a 3x increase from 2020.

Heralded as the “World’s Fastest-Growing Region For Venture Funding,” Latin America is making global waves. This is an opportunity for individual investors to piggyback.

Look at the amount of money going into late-stage & technology growth companies above and the percentage of total deals that these late-stage companies comprise of total LATAM deal volume in the chart below. LATAM companies are now maturing to the point of receiving late-stage funding and are getting to public market exits, in many cases in the U.S. Big players such as NuBank, Rappi, Nuvemshop and Loft made up about 10% of the total amount raised in the entire region in 2021. NuBank alone received $500 million from Berkshire Hathaway and has since gone public in the U.S.

We are seeing venture capital and other more institutional money aggressively looking for unicorn companies in Latin America who are, or can become, #1 in their prospective markets. They are bidding heavily to do so. The growth in capital from the early stage category was a welcome flux from previous years and shows the ability of foreign investors to begin diving into earlier deal rounds and supporting the future ecosystem of “to-be” unicorns that can provide outstanding returns.

Conclusion and Final Words:

The investment market is heating up in the Latin American market. The growth could be similar to what we saw in China decades ago that many of us missed.

Within our own portfolio companies at Legacy Group, we have seen a tremendous amount of growth in interest from our existing investor base for LATAM deals during the past year. In fact, we recently upsized our Series B offering for the Green Coffee Company by approximately 35% as a result of this increase in investor interest and opportunities for growth that we experienced at the end of 2021.

All ships are currently rising as a result of this increase in LATAM opportunities from investors, whether those investors be individuals or venture capital funds. All ranges of deals are increasing in transaction volumes whether they be seed, early-stage or later-stage companies. The funding markets are starting to enhance and sophisticate to hopefully someday mirror what exists in more developed funding markets.

On a personal level, being on the ground here in Colombia, everyday we see more talented entrepreneurs operating in the market and more accredited US-based investors looking to find exposure to Latin America based portfolio companies.

We do believe that now is the time that investors should be looking at LATAM as a serious place to allocate capital. Don’t wait twenty years before the boom has become a whimper.

We are seeing tremendous growth in the technology and fintech sectors: Latin America has systematic gaps that smart entrepreneurs can reconfigure and fill. When they do, they can build empires. We are seeing increased sophistication to the human capital focused on technology here within Colombia as digitalization becomes more embedded in early education. Within one of our portfolio companies, Polygonus, the management team has also begun recruiting outside of Colombia, targeting high-level talent in Mexico, Argentina, Peru and Ecuador to look for plentiful Latin American talent wherever it can be found.

Additionally, we are seeing more and more investors who want exposure within these sectors on an international basis. At the moment, we see these two sectors of the new economy as being at the top of the list for investor demand. Especially at early-stage company funding rounds, these are two areas for U.S. accredited investors to take particular notice of.

LATAM offers numerous legacy, family-owned companies ripe for acquisition and/or disruption: A news piece that is of particular interest in recent months in Colombia has been the potential takeover bid by Jaime Gilinski of Nutresa, one of the largest food companies in Colombia domiciled here in Medellin, Colombia. Beyond all the media hubbub, there lies a central theme to Gilinkski’s bid – he believes Nutresa, as well as many other large companies here in Colombia, are run by generational families in a manner that is less efficient than an international corporate operation. He believes it should be managed more professionally, more internationally and with less nepotism. If he wins his takeover bid, I’m sure it will be. But of more importance to international investors is to take note from this story that many companies in Latin America run in this exact same format – businesses are passed down from generation to generation, innovation becomes a sliver of what it once was, and business drags on year after year without any change. This is the capitalistic framework in which the system runs today. We believe there will be opportunities as new companies look to disrupt the “institutions” that currently exist, as well as fresh leadership that will look to move walking zombies into a new, more innovative future. We look forward to seeing both of these shifts materialize in the coming years and capturing the resulting opportunities.

About Legacy Group

Legacy Group is distinguished by a singular tradition of service to our portfolio partners; the mutual commitment to, and the seamless collaboration of, a true partnership; formidable financial and legal talent across multiple disciplines and jurisdictions; and shared professional values that focus on client needs.

We provide experience and investment to a wide range of private companies spanning many industries, including real estate, hospitality, tourism, agriculture and technology. Contact us to learn more and to discuss current investment opportunities available to you in our portfolio companies.

*This publication/newsletter is for informational purposes and does not contain or convey legal advice. The information herein should not be used or relied upon in regard to any particular facts or circumstances without first consulting a lawyer. Any views expressed herein are those of the author(s) and not necessarily those of our clients.

Sources:

https://news.crunchbase.com/news/latin-america-venture-growth-startups-2021-monthly-recap

https://finance.yahoo.com/news/green-coffee-company-funds-13-110000880.html