I can barely remember a meeting that I had with a CEO in Dubai except for one statement that he made during the meeting: “Banking is a sunset industry.” Today, over coffee and the news, this phrase resurfaced in my mind.

In April of 2012, my previous firm, PwC, engaged me to create a valuation of a business carve-out of a major international bank that was looking to potentially sell their Islamic banking unit spanning Malaysia, the United Arab Emirates and Bahrain. Even though I’ve spent the majority of my working life either analyzing financial services companies or running them, I find myself learning something new everyday in this space.

Essentially financial services companies – especially banks – are tolls on a highway. That highway is that of an efficient capitalism system, of course. Due to the nature of the relationship financial institutions have with central banks and governments, especially large American-based international banks, they have a license to print money – quite literally. They charge fees for users to engage in the daily flow of money for goods and services. In order to cross the capitalism bridge, everyone has to pay the toll.

The technology these companies use and rely on for daily operations, the SWIFT system, is largely based on technology constructed in the 1970’s and 1980’s. Anyone who tells you that banks are aggressively pursuing material upgrades to these current information systems also has some swampland in Florida to sell you at a great price. The companies are bulky and the alignment to risk/reward for company performance drives many financial institutions to take excessive risks using depositors’ or governmental funds resulting in the obvious occasional meltdown when bets go upside down; the inevitable tax-payer funded bailout always ensues.

There have been critics of the “formal” banking system over the years, and their base seems to grow with each passing day. Many of the best and brightest critics have started their own fintech companies or direct banking competitors. When these new companies “make it” they generally sell out, many times to their direct banking competitor (i.e., the old guard). The general public has recognized the inequities that exist within the current formal banking regime and have marched in the street, created Occupy Wall Street movements and, of course, whined to the “man” all to no avail. None of these groups have changed the industry in its entirety. We (by we I’m referring to the bulk of this readership as Western Nationals) live in a capitalist world. Capital drives change a lot faster than an organized walk down the south of Manhattan.

Within this article, we will aim to demonstrate that we are seeing aggressive movements of capital in the financial services sector where we see the potential for a fundamental change in the existing world order and how financial institutions of the future will need to operate in order to stay competitive. Although, on a macro-level, some of these investment amounts may appear to be miniscule, or even immaterial, they send clear messages to the global audience. Banking as we know it is already over, but this version of “Sixth Sense” will be a lot longer than 107 minutes. Bruce Willis won’t recognize his own death until many years from now.

Look at the Big Boy Bets Being Made Today

As recently reported, Warren Buffett’s Berkshire Hathaway has plowed at least $1B USD into Nubank. To most readers, and I don’t blame you for this one, you have no idea who Nubank is. To be fair, Latin American digital banks are not on every investor’s mind, but they should be. Latin America’s population is significantly underbanked. Existing institutions in LATAM are well below par when analyzed at an international level. Financial inclusion of the masses leaves much to be desired. Nubank is a great symbol of what the future of banking is likely to be.

Nubank went public on the New York Stock Exchange in December of 2021 at a valuation of approximately $50B. That’s $50 billion with a “b” by the way – they’ve made headlines as a star unicorn coming out of the region. Accolades and valuation aside, they are a purely digital bank – no physical branches, no bank tellers and no check the box forms. For readers who like to dig into the details, I encourage you to take a look at Nubank’s S-1 filing prior to their IPO. The company went from 3.8m customers in 2018 to 48.1m in Q3 2021 and are averaging 2.1m new additions per month. To put this in reference, 2.1m is almost exactly the entire population of Houston (the 4th largest city in the United States).

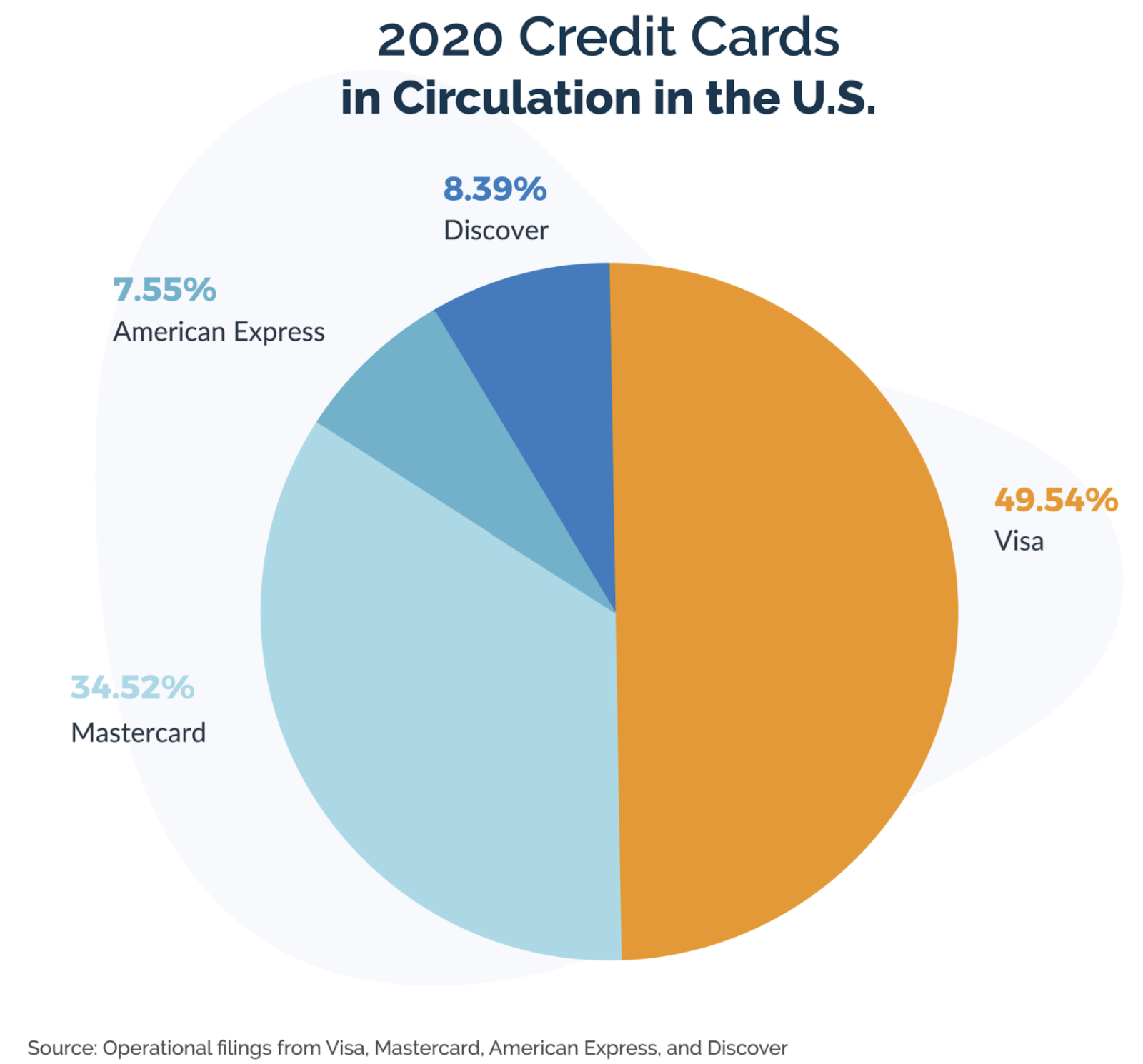

Besides that fact that everyone knows that Buffett is not a dumb guy and thinks Nubank is a smart bet, the article also goes on to say that Berkshire Hathaway “dumped $1.3 billion and $1.8 billion of Mastercard and Visa.” That is a huge statement. For anyone who is aware of the credit card industry, you’ll know that Mastercard and Visa have a complete stranglehold on the global market. Within the U.S. alone, these two control 84% of the market.

This is a duopoly in its highest form, and operating at a global scale. Running these companies should be as easy as sitting down to dinner with two CEOs and saying: “how are we all going to set market prices this year” and then just telling AMEX and Discover they better play along; job done, everyone makes a fortune. The business is perfect, or seemingly so. They charge 2 – 5% for every transaction that is used with credit cards everywhere in the world. They even charge more in some countries, where we have heard about 7% charges being prevalent. Customers don’t really have a choice whether to use them. If you are opening a new luxury restaurant and don’t take credit cards, you better be ready to take payment in dishwashing services or be ready to go out of business immediately. Cash is already dead in most parts of the world, if you can’t take digital dollars, euros or yen – your business will be the same.

Credit Card companies are an excellent example of the old guard of financial services companies. They operate on the same “toll” method as traditional banking institutions. But when one of the smartest investors in the history of the world like Buffett says (with their wallet) that they are dumping the old guard for the new one, a symbol of the future may be in place.

Digital Banks and Financial Institutions Are the Future

Without wanting to appear to be an unpaid spokesman for Nubank, I have to note one other stat here: Nubank currently services 28% of the total Brazilian population above 15 years old and they acquire 80 – 90% of their customers through word of mouth (i.e., zero customer acquisition cost and they get almost all new customers by current customers telling people how much they like them for free). For readers who aren’t familiar with Brazil, about 21% of the entire adult population doesn’t have a bank account or has one that they don’t use as they prefer the cash “black” economy. It is a perfect example of a market that the current banking system doesn’t properly address.

JP Morgan Chase by contrast, the largest bank in the United States (thereby one of the largest in the world) boasts 62 million customers, a mere 30% more than Nubank. JP Morgan Chase has been in business since 1871, Nubank since 2013. The reader doesn’t need a calculator to guess which one seems to have more growth potential. Nubank’s S-1 states that they will be going after the entire 650 million strong Latin American consumer market and are already present in Mexico, Colombia and Argentina, in addition to Brazil, where growth is already skyrocketing. Given the complacency and general apathy I see everyday in the “formal” Latin American banking sector, I fully expect that these guys have a huge runway ahead of them.

What can we learn from the above and what does this mean to the reader? Simply put: emerging wealth (i.e., usually younger, digitally-savvy customers) want everything to be digital, including financial services. They don’t want to go to physical branches to engage in banking activities, they want to access their funds in real-time, instantaneously. Banking is a chore, not a respected service to which they want a personal touch. Banks are not your friend, they are a gatekeeper to your own money. The old ways of managing money are dead. The old guard of banks and financial institutions will either evolve, or more likely buy their new-comer challengers in bulk, or they’ll be out of business in the next decade.

Conclusions and final words:

Although I don’t see the financial institutions of today going out of business tomorrow, I do see a power play that seems to be shifting everyday. It’s the same theme I saw when we were looking at brokerage company acquisitions in Hong Kong during my time in the Asia-Pacific region: brokerage fees have been a race to the bottom for the last few decades rendering brokerage firms worthless. As financial services markets become more efficient, the cost to the consumer decreases. This happens in every market, everywhere in the world. In Asia, what we saw were loads of small, family-owned brokerage firms that specialized in selling Hong Kong listed stocks via the “boiler room” scenarios the reader would be used to seeing on Martin Scorsese’s version of the Wolf of Wall Street. How do you compete with Etrade, Fidelity, Scottrade, etc. which are doing equity trades for a few bucks a trade, or potentially for free in today’s world? The short answer is: you don’t, you go out of business. The same will happen with banking services, as digital banks emerge: fees to the customer will ultimately decrease as competition ensues and only banks with low platform costs (most likely the digital variety) will be able to compete and survive.

Latin America is primed for multiple fintech revolutions: Nubank is only one example of the digital revolution of the financial services market that is gripping the world. Their growth demonstrates the undeniable demand for digital services from today’s banking clientele. But, Nubank’s product portfolio is ultimately limited – its focus is consumer banking and small and medium enterprise (SME) banking. There are numerous other financial services markets that are wide open such as: private banking, large corporate banking, insurance products, trust structuring & servicing, public and private market securities brokerage, etc. All these markets could be considered somewhat inefficient in developed markets. Within Latin America, expect that the current service providers use the equivalent of an abacus to calculate your payment schedules.

We at Legacy Group are seeing significant movement from talented entrepreneurs trying to solve various gaps that exist in the LATAM market within the financial services space. Honestly, if we only focused on Fintech over the next decade, we would not need another industry vertical to find interesting portfolio companies to place capital into. Expect that we will present several interesting opportunities in LATAM fintech for accredited U.S. investors over the next several years.

About Legacy Group

Legacy Group is distinguished by a singular tradition of service to our portfolio partners; the mutual commitment to, and the seamless collaboration of, a true partnership; formidable financial and legal talent across multiple disciplines and jurisdictions; and shared professional values that focus on client needs.

We provide experience and investment to a wide range of private companies spanning many industries, including real estate, hospitality, tourism, agriculture and technology. Contact us to learn more and to discuss current investment opportunities available to you in our portfolio companies.

*This publication/newsletter is for informational purposes and does not contain or convey legal advice. The information herein should not be used or relied upon in regard to any particular facts or circumstances without first consulting a lawyer. Any views expressed herein are those of the author(s) and not necessarily those of our clients.

Sources:

https://www.swift.com/about-us/history

https://finance.yahoo.com/news/warren-buffett-invests-1b-bitcoin-011723509.html

https://www.politifact.com/largestcities/

https://www.managementstudyguide.com/mastercard-visa-duopoly.htm

https://en.wikipedia.org/wiki/The_Wolf_of_Wall_Street_(2013_film)

https://en.wikipedia.org/wiki/J.P._Morgan_%26_Co.

https://www.sec.gov/Archives/edgar/data/0001691493/000119312521314359/d213207df1.htm