Two of the largest capital allocators in the world – insurance companies and pension funds – are making conscious efforts to migrate larger chunks of their portfolios into two specific sectors: climate-focused investments and alternative assets.

Why is this important to our accredited high-net-worth-investors?

A recent example is that of Calpers (the California Public Employees’ Retirement System). Calpers has recently announced that it will include more alternative assets in its portfolio, and will even borrow to do so.

As reported by the Wall Street Journal, U.S. pensions are hundreds of billions of dollars in the red on their future pension obligations. How can pension funds possibly close this gap in a market environment where yields are so hard to find? What is Calpers and others like it to do?

The Calpers trustees voted to increase its position in higher-yielding, alternative investments to 13% from 8% and will add a 5% allocation to private debt. A similar example is the Ohio School Pension Fund. Their solution was the same – turn to alternative investment options to fill their yield gaps.

In a recent survey, BlackRock, the world’s largest asset manager, spoke with 362 executives at insurance companies representing investment portfolios across 26 markets. More than one in three respondents now see environmental concerns as a potential headwind and where they need to be making capital placements over the next two years.

The major investment themes for insurers this year include a growing emphasis on sustainable companies and the need for diversification into higher-yielding alternative investments. Stated simply, their directive is to participate more heavily in the growth of investments directly into private markets.

If the big players in the institutional finance world are turning to alternative and sustainable investments should you be as well?

How much capital are we talking about here?

Although not all investors will immediately recognize the capital power that both pension funds and insurance executives have at their fingertips, some simple math will quickly explain the gravity.

Assets under management (AUM) of the world’s top 300 pension funds increased by 11.5% to a total of US$21.7 trillion in 2020, according to the annual research conducted by the Thinking Ahead Institute. The California Public Employees’ Retirement System, referenced above, represents $495 billion alone. Of the insurance survey BlackRock performed as described above, these 362 insurance company executives control more than $27 trillion in investable assets all over the world. Keep in mind that these numbers are just the top pension funds and a selection of the top insurance companies, not the entire breadth of both industries. The actual assets under management of each of these two groups only gets harder to fathom.

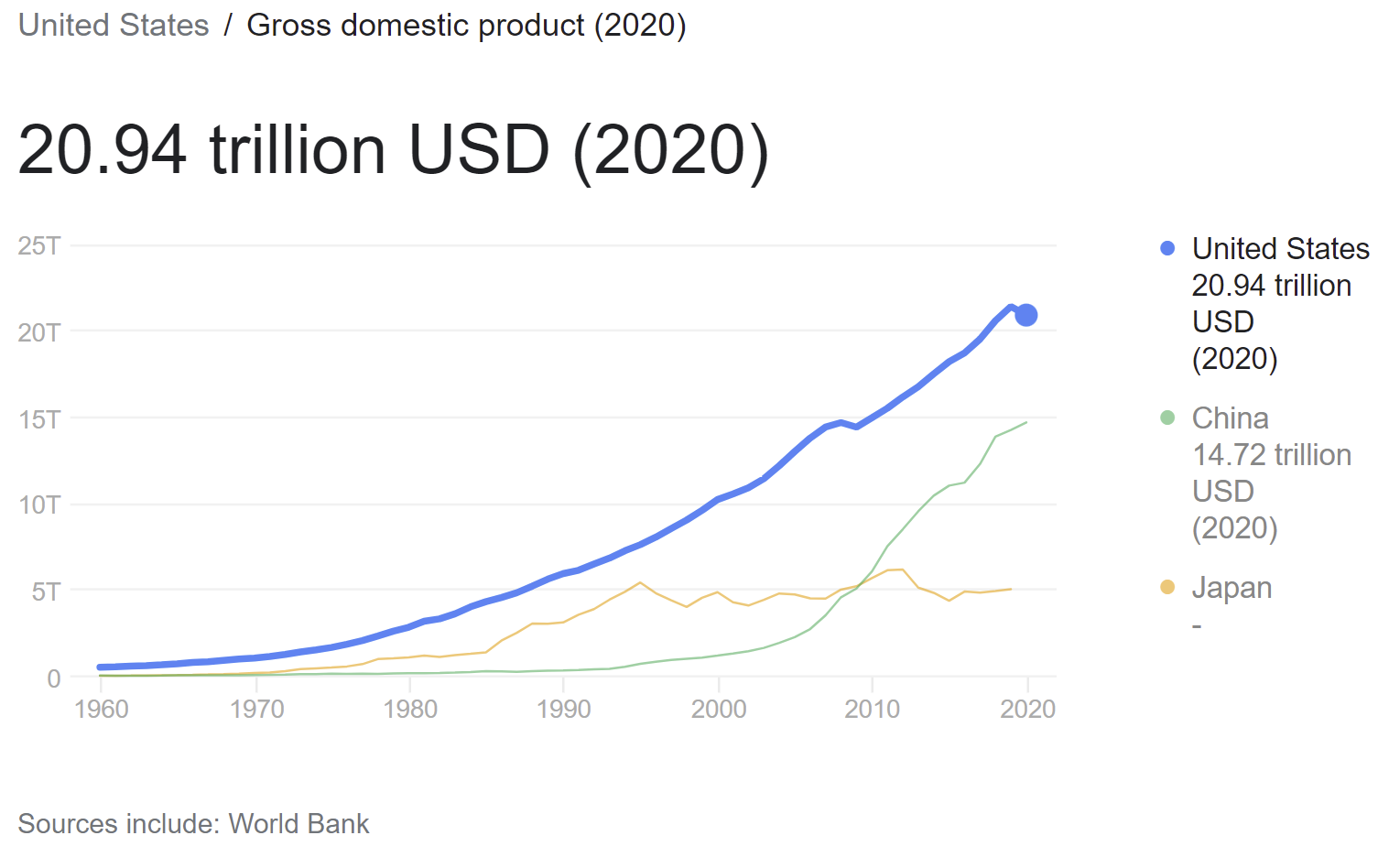

Let’s further put these numbers into perspective. The GDP of the entire U.S. economy in 2020 was almost $21 trillion. Both top pension funds and top insurance companies, controlling $21.7 trillion and $27 trillion, respectively, are therefore now each managing capital in excess of the United States´ total annual GDP.

There is a lot of capital here that needs to be moved to assets with meaningful yields.

What is an estimate of the amount of capital that could be moving into alternative investments?

Given the figures above, between pension funds and large insurance companies there is almost $50 trillion currently in play in terms of total capital managed and to be deployed.

Let’s assume that these groups will also migrate more heavily to alternative investments in line with the Calpers allocation methodology we described. This assumption is reasonable as yields in public equities become more out of reach, commercial real estate struggles to produce in a meaningful way and most high-yield debt is under water due to our current inflationary environment. Follow-the-leader as well is often, for many, a reasonable investment strategy.

Therefore, per the above, we expect that pension funds and large insurance companies will allocate an extra 5% into private equities and another 5% into private debt, for a total of a 10% overall portfolio reallocation to alternatives. Without accounting for any growth within either of these capital pools, this would result in $5 trillion, or roughly three times the GDP of Texas, of new money being thrown at the alternative investment industry in the near-term. A big number.

To put this $5 trillion figure further into perspective, the entire alternative investment industry is currently only expected to include $11.8 trillion of investment by the end of 2021. This $5 trillion additional anticipated inflow from pension funds and insurance companies in the coming years would result in the alternatives industry growing over 40% from just these investment sources. Substantial growth of investment into alternatives is coming.

Should you care as a high net worth accredited investor?

Conclusion and Author’s Final Words:

This latest round of news is just another reinforcement that alternative investments are going to continue to heat up in the coming years. Institutional money managers are not able to keep up with their yield and total return requirements from traditional investments as provided by public markets so they must evolve to meet their clients´ needs (and to stay in business).

This will have several ramifications for accredited individual investors:

Expect that institutional investors will start to participate more, and compete directly with individual investors, within mid-sized private placement offerings.

We have seen this activity first hand at Legacy Group from some of the smaller pension funds that have been kicking tires related to our recent Green Coffee Company Series B Offering. Through our discussions with fund managers, we believe that these funds are targeting opportunities where they can (1) place $30 million and up and (2) where the companies they invest in have a strong element of impact and sustainability in their business model.

Expect that groups like pension funds and insurance companies will start to compete at these historically lower levels of capital deployment as they build more sophisticated asset management teams that are focused on finding alpha within the private investment space.

As these firms compete and provide more capital to the available pool, expect that valuations of solid private companies will rise and total return rates for individual investors will potentially go down in future funding rounds.

Long story short, now is the time to be investing in alternative assets that you come across before prices go up. In the coming years, it is reasonable to assume that total returns may come down as floods of outside institutional capital are added to the market and returns on equity become more challenging. It is a good time to have your eyes open for opportunity. Get in early and then let these large capital allocators get you the returns that you desired as they piggyback on your early investment and drive higher and higher valuations towards exits.

This capital group will rarely compete at very early stage funding rounds. You can beat them to the show.

Due to the swath of capital that these institutional investors need to manage, they very rarely, if ever, will analyze opportunities requiring investments of less than $10 million. Moreover, these funds are often in “incremental wealth creation” or “preservation” mode, which naturally leads them to wait to invest in companies until later in their life cycles where financial metrics are more predictable and proven.

This reluctance creates opportunity for individual investors who are looking for long-term total returns and are properly prepared for the inherent risks of early stage company investing. Over the next several years, we find it likely that it will be extremely challenging for individual investors to participate in later stage funding rounds like Series D, E and pre-IPO in successful growing companies. Institutional investors are likely to swallow those rounds whole. Individual investors should look to earlier funding rounds unless they individually have high seven- or eight-figure checks that they can place into individual portfolio companies at later stages and can compete with large institutions.

For those who are looking at six-figure checks like most accredited investors, look at Seed, Series A and B rounds of top emerging companies as potential future gold mines for your investment portfolio.

We will keep working here at Legacy Group to bring you those opportunities.

About Legacy Group

Legacy Group is distinguished by a singular tradition of service to our portfolio partners; the mutual commitment to, and the seamless collaboration of, a true partnership; formidable financial and legal talent across multiple disciplines and jurisdictions; and shared professional values that focus on client needs.

We provide experience and investment to a wide range of private companies spanning many industries, including real estate, hospitality, tourism, agriculture and technology. Contact us to learn more and to discuss current investment opportunities available to you in our portfolio companies.

*This publication/newsletter is for informational purposes and does not contain or convey legal advice. The information herein should not be used or relied upon in regard to any particular facts or circumstances without first consulting a lawyer. Any views expressed herein are those of the author(s) and not necessarily those of our clients.

Sources:

https://datatopics.worldbank.org/world-development-indicators/

https://www.fool.com/research/high-net-worth-alternative-investments/