For the first time in over a decade, inflation rates in the U.S. economy surpassed 5% for May through August of 2021. As supply-chain troubles, post-lockdown demand surges, skyrocketing commodity prices, and increased federal spending continue, economists around the world are sounding the alarm bells that inflation will likely accelerate throughout the end of 2021. While the verdict is still out as to whether this phenomenon is the global economy’s new normal, many high net worth investors (“HNWIs”) we have talked to are on the lookout for inflation hedges in order to manage that risk.

Why are land and agriculture good inflation hedges?

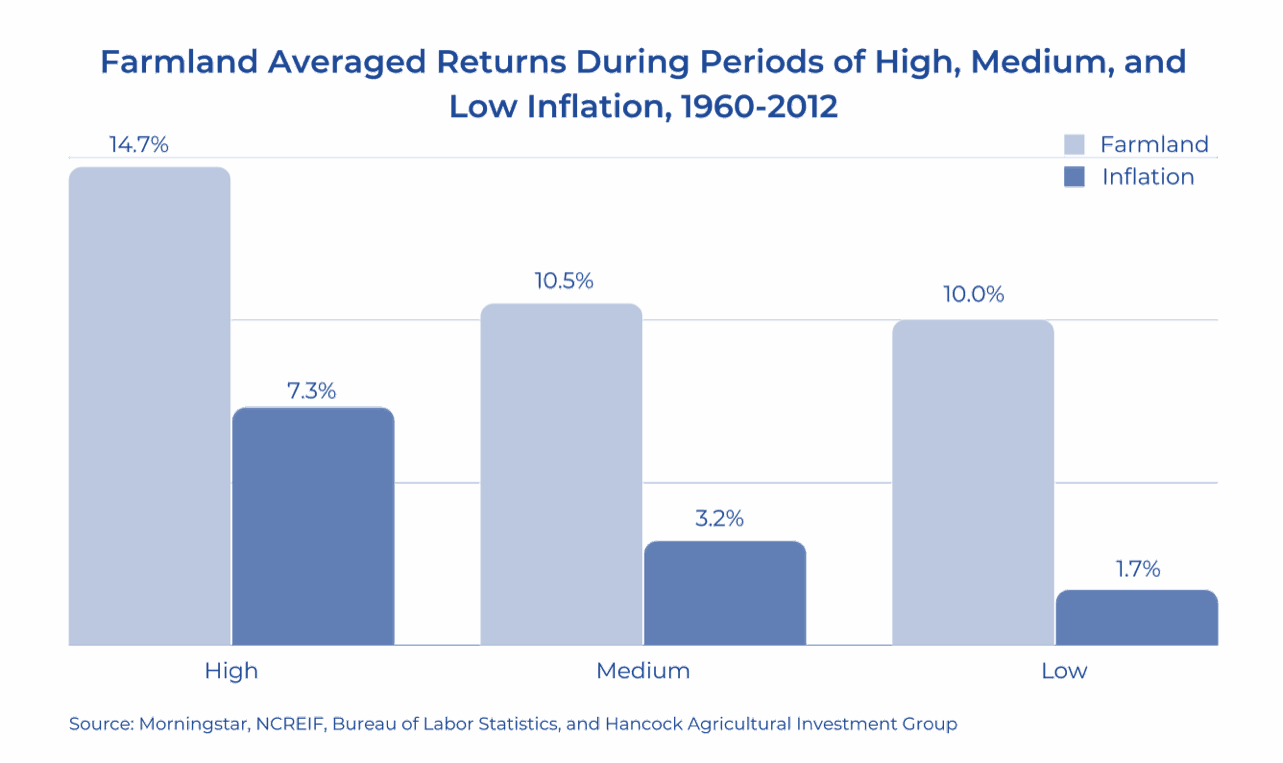

Many of our readers may already be well-versed in inflation hedging assets like farmland and agriculture. Unlike many other asset classes that run the risk of losing value during inflationary periods, land and other real assets are known for maintaining their value in the face of a decline in purchasing power. In fact, according to a University of Illinois study, land is tightly correlated with the Consumer Price Index (CPI), commonly used as a metric for inflation. As inflation rises, land values tend to rise as well. This tendency can be seen in action in the chart below. The chart portrays how land has actually generated higher returns on average in times of inflationary pressure.

Favorable Trends

Why might increases in the CPI correlate with higher farmland returns? Well, because inflation most commonly leads to rising commodity prices. Think of a food staple like corn or coffee. Farmers are increasing their revenue streams in line with that rise, which is indirectly linked to appreciated land valuation. When farmers can charge more for their goods, the value of the land that produces those goods rises. This speaks to one of the additional added benefits of farmland over other inflation hedges like gold. Unlike gold, with farmland the real asset not only increases in value, but itself generates recurring income through the production of goods and is actually productive.

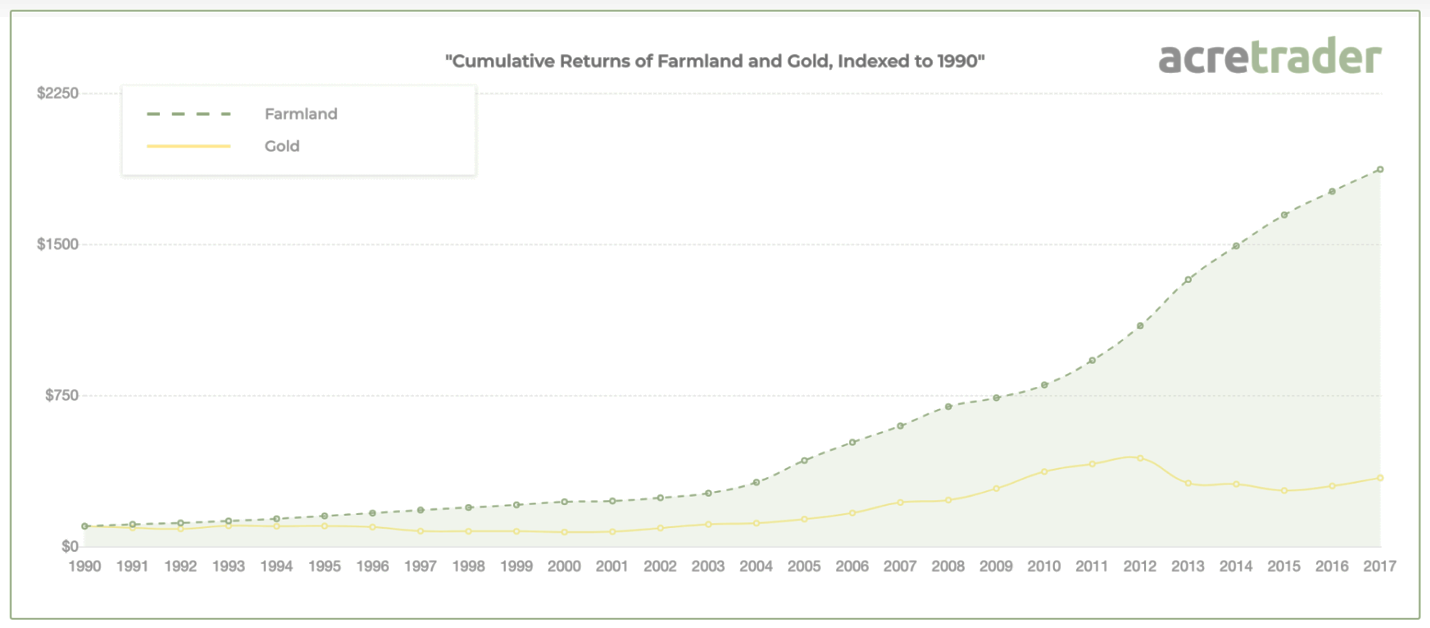

This correlative effect is not the only benefit land has over gold and other non-productive assets when thinking about how to hedge against inflation. Another area is in market performance and volatility. You can see below a chart displaying cumulative returns of farmland and gold over the past three decades. The chart clearly illustrates the limited volatility and better financial performance of farmland in comparison to gold over that three decade period.

Supply and Demand

Another way to view farmland’s stable real value comes down to whether you believe supply and demand for farmland will increase or decrease in the long-run. From our perspective, it is evident that demand for farmland investment will only be increasing as supply wanes. The Food and Agricultural Organization of the United Nations reports that by 2050, we will need to increase food production by over 50% in order to feed our growing and more prosperous global population. At the same time, land repurposed for human use is decreasing the available supply of farmland. These two factors have profound implications on the responsibility and pressure for farmers and agricultural companies to innovate. It will also inherently drive up the value of arable land and the companies that specialize in the land management, infrastructure and agricultural assets to satisfy this growing demand. This can be good news for investors interested in investing in farmland and agriculture.

What are global investment leaders doing in farming and agriculture?

“I needed no unusual knowledge or intelligence to conclude the investment had no downside and potentially had substantial upside,” – Warren Buffett, letter to Berkshire Hathaway shareholders regarding farmland acquisitions

“I believe that agricultural land, productive agricultural land, with water on site will be very valuable in the future, and I have put a good amount of money into that,” said Michael Burry, in an interview with Bloomberg.

How have these characteristics of farmland investing manifested in decision-making from wealthy investors? In 2019, the top 100 landowners in the U.S. personally owned over 2% of all land in the U.S. That number is up 50% from a decade earlier. One of the new names on that list was Bill Gates, who became the country’s largest owner of farmland in 2021 with over 242,000 acres to his name. Bill Gates’ investment in farmland is in line with other high-profile investors like Warren Buffett, who has described land as an “investment with no downside and potentially substantial upside”.

Buffett is also famous for his distaste of gold, cryptocurrencies and other non-productive assets as investments. He once commented in an interview when presented with a choice between owning all the gold in the world or all the farmland in the U.S. to, “call me crazy, but I’m taking the land.”

Challenges of investing in farmland

While there are many benefits to farmland investments, the asset class is notoriously difficult to access for investors. It may be easy for ultra-high-net-worth individuals (UHNWIs) and institutions to purchase huge swaths of land. But, for the average investor, being a 100% owner of a piece of productive farmland is often not feasible. Below is a table laying out some of the key challenges a typical investor, even high-net-worth individuals (HNWIs) who want exposure to farmland, face when investing in farmland.

| Investment Mechanism | Description | Challenge |

| Traditional Private Equity Investment | Multi-billion dollar investment vehicles in large landholdings run by a management team at industrial scale | -High investment minimums (~$1 million USD at least) -Zero control over where the capital is placed and which assets are purchased -Traditionally high fees |

| Farmland REIT | Retail investor-accessible opportunity to invest in landholdings through public markets | -Very limited transparency with investments -Returns often still correlated to general market swings and those swings often are correlated to inflation concerns |

| Agriculture Stocks | Investors purchase stocks in publicly traded companies with farmland or agriculture sector exposure | -Not actually direct exposure to farmland -Ag stocks are correlated with general market movements -Current valuations on public markets are at historical highs |

| Direct Ownership | Investors own and manage their own farm | -High investment minimum – at least $10 million for any meaningful farmland investment -Actively managing land is time consuming and expertise in agriculture is a necessity |

As you can see, the current availability for true exposure to farmland investment opportunities that can actually serve as a hedge against inflation can be very difficult for private U.S. investors due a confluence of variables. Institutional investors have made it difficult even for HNWIs to participate without making an 8-figure placement in a fund or competing directly against them in any potential acquisition scenario. The Farmland REITs have seen increases in value following the COVID-19 pandemic, but if their historical performance is any indication, it is unlikely that growth can be maintained going forward. At the same time, the stock market is continuing to hit record numbers, and it is unclear if the valuation multiples for publicly traded companies are truly sustainable. This has caused many of the HNWIs in our network at Legacy Group to diversify outside of the U.S. into agricultural investments that are denominated, or readily transactable, in US Dollars – like our portfolio company, The Green Coffee Company (“GCC”).

How to Hedge Inflation with a Farmland Investment

We have a solution. At Legacy Group, we have developed our own method of building attractive investment opportunities in farmland and the agricultural sector for investors. Our business-building strategy can be broken down into a few primary themes:

- Focus on markets in developing countries that are better positioned to earn outsized returns compared to the oversaturated U.S. market.

- Target farmed agricultural products that are highly liquid and transactable due to significant global demand, like coffee.

- Product sales should be done in USD to act as an effective hedge for US investors. A focus on the United States as the target end market for products is preferable.

- Use multinational corporate structures for investors with headquarters in the United States so that our businesses have multiple exit opportunities (private sale or U.S. IPO), investors get all the benefits of U.S. law around their investment and so that the investment process is frictionless.

We are, for example, very excited by what the Green Coffee Company (“GCC”) can offer our investors who are searching for options to use land as an inflation hedge and earn outsized financial returns.

The GCC is our Colombia-based coffee company that is currently a Top-3 producer of coffee in all of the country of Colombia. The GCC’s primary assets – coffee farms and processing equipment – provide direct exposure to farmland and agriculture for HNWIs. New investment in state-of-the-art technology, tree-buildout and additional land acquisitions over the past few years have effectively positioned GCC for outsized financial returns for our investors (projected 48% IRRs). Both the coffee the GCC sells and all investment in the business are denominated in US Dollars, meaning exposure to other risk factors that typically come with emerging market investments are limited. Finally, with lower investment minimums than traditional private equity, the GCC actually provides HNWIs the chance to participate in this exciting and timeless coffee industry.

With GCC’s planned IPO following an expansion into the U.S. markets in the coming years, the opportunity for high returns from consolidated farmland investment has never been more clear. If you would like to learn more about investing in the Green Coffee Company and how to hedge inflation with an investment in productive agriculture, please reach out to us at investor.relations@legacy-group.co. More information about the investment opportunity can also be found here.

Conclusion

Is land a good hedge against inflation? Is an investment in farmland right for your hedge portfolio? Investing in farmland and agriculture is without question one of the best investments to hedge against inflation. Moreover, farmland used in agriculture is a productive asset that can generate cash flow and appreciation for its investors over the course of the investment. This list of benefits makes an investment in productive farmland a strong investment option for any portfolio and for battling ongoing inflationary concerns.

About Legacy Group

Legacy Group is distinguished by a singular tradition of service to our portfolio partners; the mutual commitment to, and the seamless collaboration of, a true partnership; formidable financial and legal talent across multiple disciplines and jurisdictions; and shared professional values that focus on client needs.

We provide experience and investment to a wide range of private companies spanning many industries, including real estate, hospitality, tourism, agriculture and technology. CONTACT US to learn more and to discuss current investment opportunities available to you in our portfolio companies.

*This publication/newsletter is for informational purposes and does not contain or convey legal advice. The information herein should not be used or relied upon in regard to any particular facts or circumstances without first consulting a lawyer. Any views expressed herein are those of the author(s) and not necessarily those of our clients.